When investors first add digital assets to their financial plan, a practical question often arises: Where should I keep my crypto?

There are two common routes that typically surface:

- A standard exchange wallet (custodial, typically hot wallet access) for convenience and trading speed.

- A crypto IRA custodian (regulated retirement account) for tax advantages and institutional-grade custody.

Both paths are custodial, but their governance, security, tax treatment and intended use differ a lot. Understanding those differences can help investors decide whether their priority is intraday trading agility or retirement-grade structure—or a blend of both.

This guide unpacks how exchange wallets and crypto IRA custodians compare across ownership and control, security and regulation, fees, liquidity and taxes, then offers an actionable framework for making a choice.

Understanding the building blocks

What is a standard exchange wallet?

A standard exchange wallet is a custodial wallet provided by a centralized crypto exchange. The exchange manages key material and signs transactions on your behalf. Most balances earmarked for trading and quick withdrawals sit in hot wallets (online), with the majority of platform reserves typically in cold storage.

Pros:

- Frictionless buying, selling and transferring.

- Simple account recovery (no seed-phrase management).

- Depth of markets and order types for active traders.

Cons:

- “Not your keys, not your coins”: you rely on the exchange’s security and solvency.

- Hot-wallet exposure increases the attack surface.

- Not tax advantaged like retirement-accounts.

What is a crypto IRA custodian?

A crypto IRA custodian is a regulated entity that holds retirement assets in trust for account owners. The custodian’s job is to safeguard assets and ensure compliance with tax and retirement laws (e.g., contribution limits, prohibited transactions, required minimum distributions (RMDs) for certain accounts).

Pros:

- Institutional-grade custody (heavy use of cold storage, multi-sig, segregation).

- Tax-deferred or tax-free growth depending on the IRA type.

- Assets are held within a legal trust/custodial structure for retirement.

Cons:

- Trading is not as instantaneous as an exchange hot wallet.

- Retirement account workflows (paperwork, approvals) can add steps.

- Fees may include trade spreads and/or custody/administration charges.

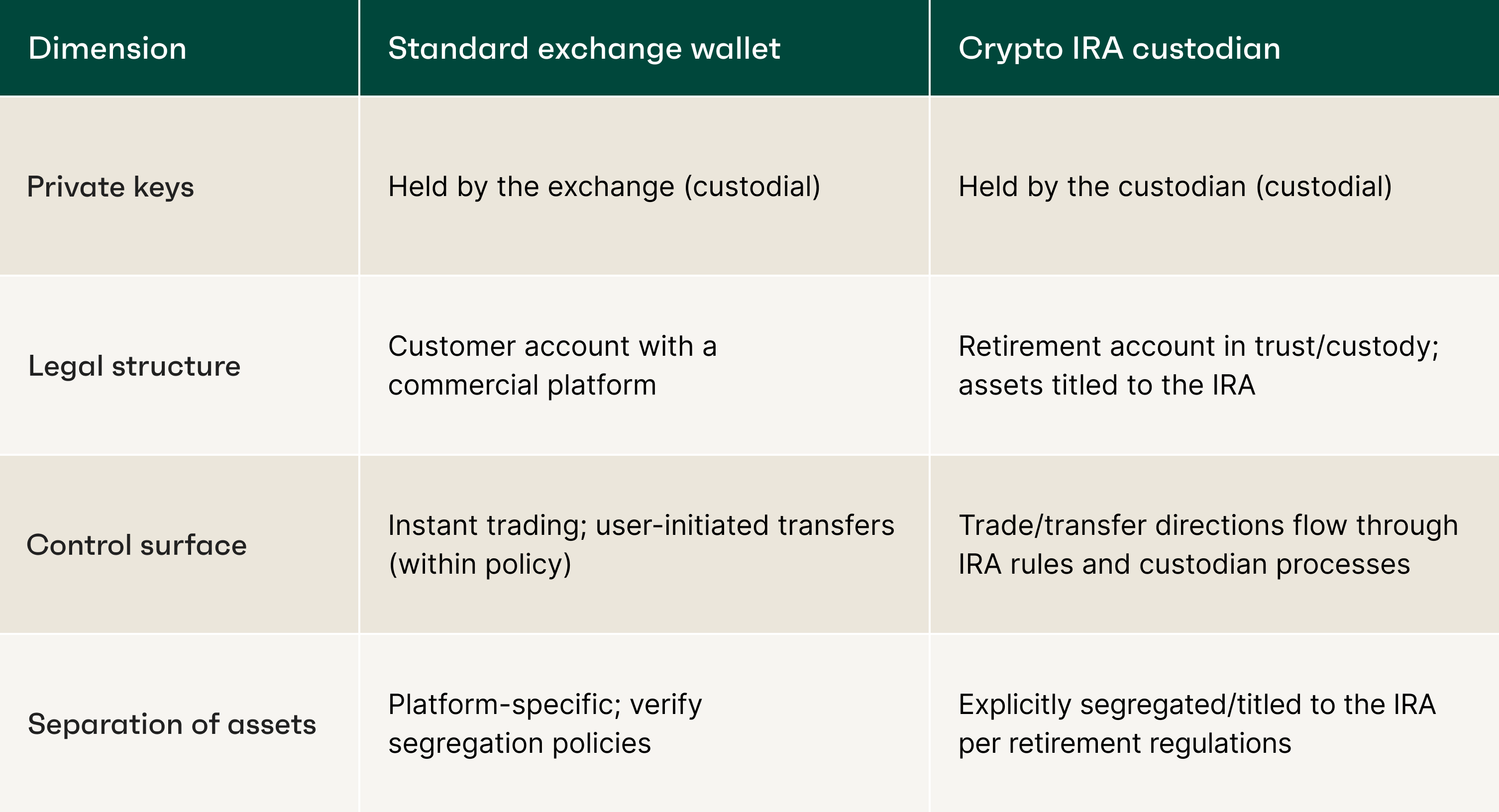

Ownership & control: Who Holds the keys and how?

Takeaway: Both models are custodial, but a crypto IRA wraps legal ownership in a retirement trust/custody structure, whereas an exchange account is a commercial service relationship. That legal wrapper matters for asset segregation, reporting and beneficiary planning.

Security: Where and how crypto is stored

Security design differs because the use case differs.

Custody models

- Exchanges: Blend of hot (for speed) and cold (for reserves) storage. Emphasis on liquidity and throughput for high trading volumes.

- Crypto IRA custodians: Heavy reliance on cold storage, multi-signature approvals, geographic key distribution and role-based access. Emphasis on long-term safeguarding.

Typical safeguards to look for

- Key management: HSMs, split-key/threshold signatures, multi-sig.

- Cold storage allocation: Majority of balances stored offline.

- Operational controls: Segregation of duties, transaction whitelists, withdrawal velocity limits.

- Independent audits: SOC 1/2/3, ISO/IEC 27001, independent penetration testing.

- Insurance & banking: Clear disclosures—crypto itself is not FDIC/SIPC insured. (USD cash balances at insured banks may be eligible for FDIC coverage up to legal limits; policies vary.)

- Incident response: Documented plan, user notifications, post-mortems.

Bottom line: In general, exchanges optimize for speed while IRA custodians optimize for safety. Investors should determine which they value more based on the specific assets and timeframe in question.

Regulation & compliance: The guardrails

- Exchanges typically operate with AML/KYC programs, MSB registration where applicable and government oversight varying by jurisdiction and business scope.

- Crypto IRA custodians add a retirement account compliance layer: contributions, rollovers, reporting, prohibited transactions, beneficiary handling and (for certain accounts) RMDs—all within federally recognized custody/trust arrangements.

This additional compliance is a feature, not a bug. It’s designed for long-horizon funds where tax treatment and beneficiary planning are critical.

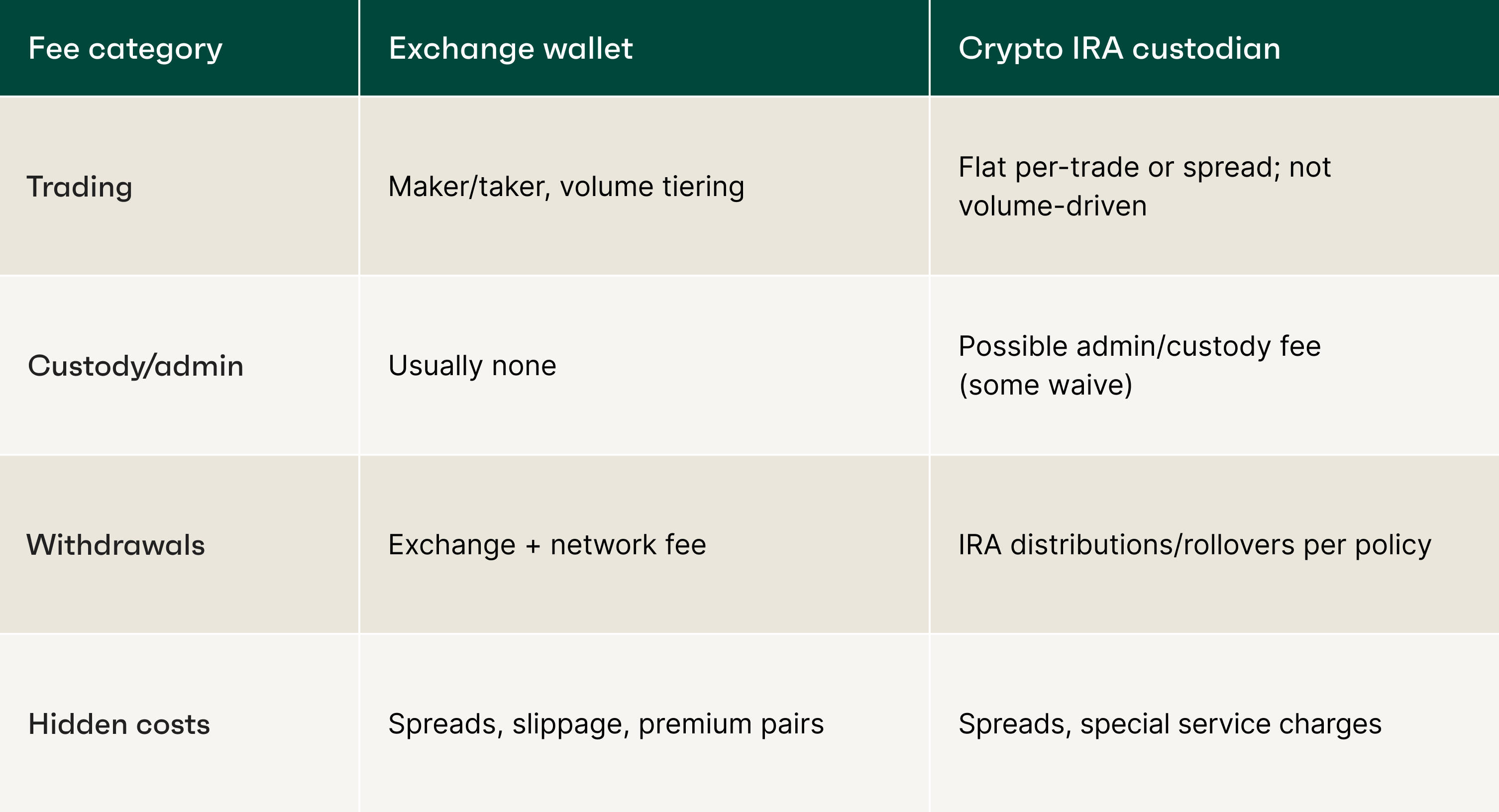

Fees & costs: What you’ll pay for

Common exchange wallet fees

- Trading fees: Maker/taker schedules; volume-tiered discounts.

- Spread: Difference between buy/sell quotes; sometimes larger than the posted fee.

- Withdrawal fees: Exchange-set plus network fees.

- Deposit fees: For specific payment rails (e.g., cards, certain wires).

- Network fees: Blockchain miners/validators; variable.

Common crypto IRA fees

- Trading fees/spreads: Often a flat trade fee or spread; check the schedule.

- Custody/admin: May be flat (monthly/annual) or % of assets; some providers waive admin fees but charge per trade.

- Funding/rollover: Typically low/no fee; verify.

- Miscellaneous: Paper checks, express wires, special handling (varies).

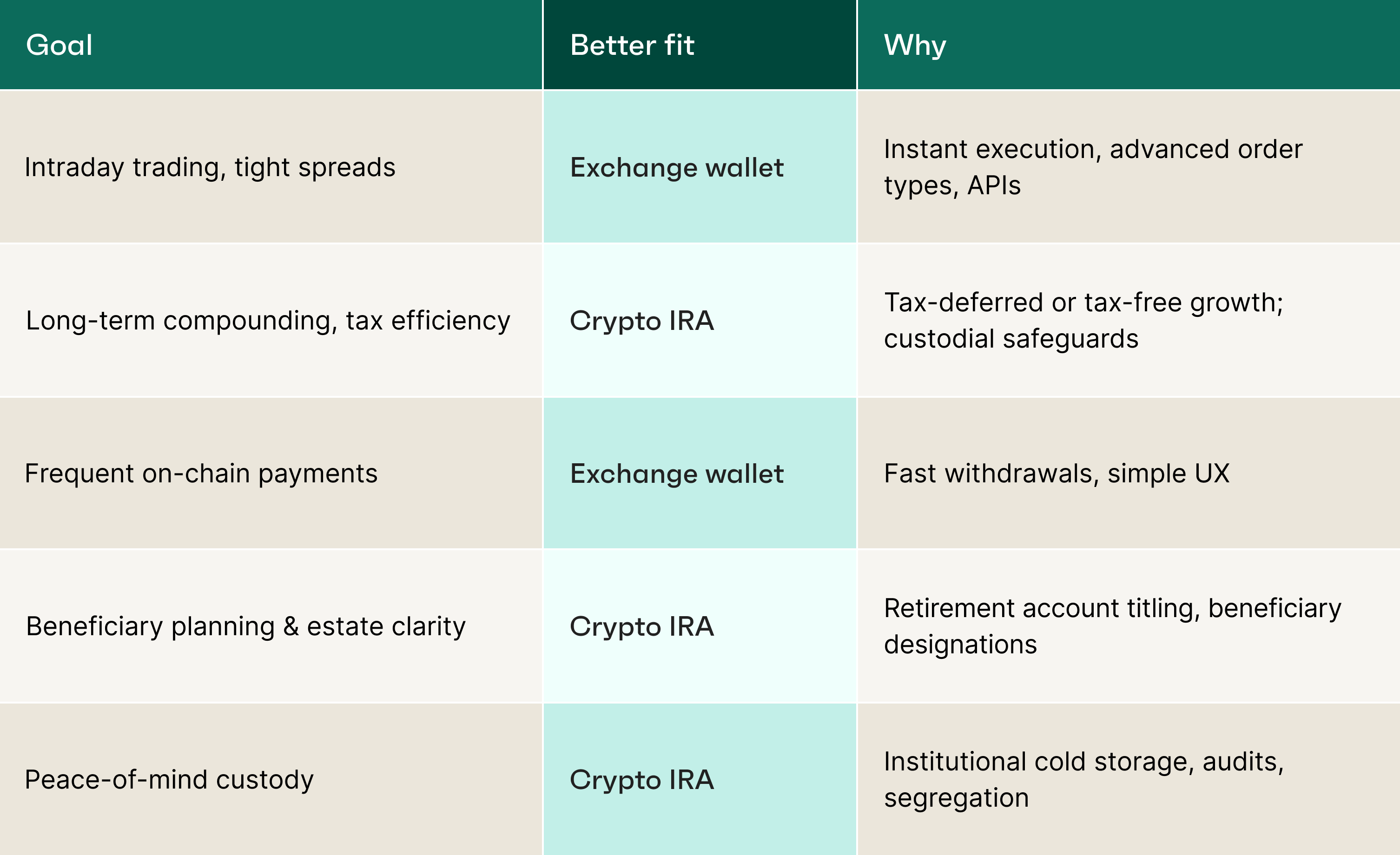

Liquidity & workflows: Access vs. process

- Exchange wallets: Built for immediacy—market/limit orders, quick withdrawals, API trading and frequent rebalancing.

- Crypto IRA custodians: Built for process integrity—trade requests, settlement within custodian/exchange partners and compliance checks on movements (especially distributions or rollovers).

For day-traders, an exchange wallet’s immediacy can be essential. For retirement savers, slower, documented workflows are usually acceptable because they are optimizing for structure and tax efficiency rather than split-second fills.

Taxes: The deciding factor for many

Exchange wallet (taxable)

- Every sale, swap or spend is a taxable event (capital gains/losses).

- Short-term gains (≤ 1 year) taxed at ordinary income rates; long-term (> 1 year) at capital gains rates.

- Requires meticulous recordkeeping (cost basis, holding periods, proceeds).

Crypto IRA (tax-advantaged)

- Trades inside the IRA are not currently taxable.

- Traditional/SEP IRA: Potentially tax-deductible contributions; taxes due on distributions in retirement.

- Roth IRA: After-tax contributions; qualified distributions are tax-free (subject to age and seasoning rules).

- No capital gains reporting for each trade; simplified annual reporting.

Implication: If the goal is decades-long compounding, a crypto IRA’s tax shield can substantially change the ending balance compared to a taxable account, even if fees are slightly higher.

Important: This is general information, not tax advice. Always consult a qualified tax professional.

Use case fit: Trading desk vs. retirement plan

Practical scenarios

- The Active Trader (Aisha)

Aisha rebalances daily and uses stop-limits. She keeps a working balance on an exchange wallet, with the majority of her long-term crypto exposure in a Roth crypto IRA to capture tax-free growth. - The Long-Horizon Saver (Marco)

Marco dollar-cost averages into BTC and ETH monthly and doesn’t need instant exits. He directs contributions into a Traditional crypto IRA, appreciates the admin support and ignores daily volatility. - The Hybrid Allocator (Priya)

Priya runs a barbell: a small, speculative sleeve for new tokens on exchange; the core of her digital assets in a crypto IRA. She rebalances the IRA quarterly to maintain target weights.

Due diligence checklist (both models)

Security & custody

- Cold-storage percentage disclosed?

- Multi-sig/key sharding/HSMs used?

- Segregation of client assets? Proof of reserves or attestations?

Compliance

- AML/KYC policies, sanctions screening, transaction monitoring?

- Retirement account expertise for IRAs (contributions, RMDs, rollovers, prohibited transactions)?

Audits & standards

- SOC 2/SOC 3 reports? ISO/IEC 27001? Pen tests?

- Incident response and public post-mortems?

Fees & disclosures

- Full, plain-English schedule (trading, custody, withdrawal, spreads)?

- Example cost walkthroughs?

Operations & support

- Settlement times; withdrawal limits; whitelists?

- Human support for rollovers, beneficiary updates and distributions?

Risk considerations

- Platform risk: Exchange insolvency/events; IRA custodian or sub-custodian failures (mitigated by segregation and audits).

- Security risk: Hot-wallet compromises, phishing, SIM swap; IRA cold-storage mitigates but doesn’t eliminate risk.

- Regulatory risk: Rules evolve; ensure provider adapts (especially for staking, derivatives or new asset types).

- Liquidity & market risk: Bid-ask spreads, slippage; tax-shielded IRAs encourage longer horizons that smooth volatility.

- Operational risk: Transfer errors, address whitelisting, human mistakes; process controls matter.

Building a smart mix

Many investors adopt a two-bucket strategy:

- Tactical bucket (exchange wallet): A small allocation for active trading, quick exits and experimental assets.

- Strategic bucket (crypto IRA): A larger, rules-driven allocation for core holdings (e.g., BTC/ETH), targeting long-term, tax-efficient compounding.

This approach pairs agility with structure, matching the strengths of each model to the job investors need them to do.

Step-by-step: Moving from exchange to crypto IRA

- Choose IRA type: Traditional, Roth, or SEP—align with tax outlook and eligibility.

- Select a custodian: Verify licenses, custody model, supported assets, fee clarity and audit posture.

- Fund the account: Annual contribution, IRA-to-IRA transfer or rollover from a qualified plan (mind the rules and timelines).

- Set a strategy: Define target allocation, DCA schedule and rebalance cadence (e.g., quarterly).

- Execute & monitor: Place orders via the custodian’s platform; review statements and confirm storage/audit updates.

- Keep records: Beneficiaries, contributions, and any required forms—the custodian should guide you.

Common myths (debunked)

- “I need self-custody for an IRA.”

IRAs require a qualified custodian/trustee; you don’t hold the keys personally in a compliant IRA. - “Crypto in an IRA is risk-free because it’s regulated.”

Regulation reduces certain risks (custody, reporting) but doesn’t remove market or operational risk. - “Exchange wallets are unsafe by default.”

Leading exchanges invest heavily in security. The real question is whether their risk profile matches your time horizon and objectives.

Conclusion

Evaluating standard exchange wallets against crypto IRA custodians boils down to aligning tools with goals:

- An exchange wallet may be optimal when speed, order flexibility and frequent transfers matter most.

- A crypto IRA custodian could be the best fit when you want retirement-grade custody, clear legal ownership and powerful tax advantages to amplify compounding.

Plenty of investors use both: a nimble trading sleeve for tactics and a tax-advantaged IRA core for strategy. Whichever path you pick, insist on transparent fees, independent audits, robust custody controls and support that actually helps.

Note: This article provides general information and is not tax, legal or investment advice. Before making decisions about IRAs or digital assets, consult a qualified tax advisor or financial professional.

FAQs

Can I access my private keys in a crypto IRA?

No. A qualified custodian must hold IRA assets. You direct investments, but the custodian controls keys to maintain compliance and safeguard the account.

Are crypto assets in either model FDIC or SIPC insured?

No. Crypto itself is not FDIC or SIPC insured. USD cash balances held at insured banks may be FDIC-eligible up to legal limits; check your provider’s disclosures.

Do crypto IRAs support staking or yield features?

Some do, under strict policies. If offered, rewards typically accrue inside the IRA and follow IRA tax treatment (e.g., tax-deferred or tax-free at qualified distribution). Availability, risks and controls vary—review carefully.

What if I want both speed and tax advantages?

Use a hybrid approach: Maintain a smaller trading sleeve on an exchange, with the long-term core in a crypto IRA. Rebalance on a schedule, not emotions.

How do fees compare in practice?

Exchanges often win on per-trade costs for active users; IRAs win on lifetime tax efficiency if you hold for years. Model your behavior (trades/month, ticket size, holding period) and compare after-tax outcomes.